Page 1

Loading page image...

Page 2

Loading page image...

Page 3

Loading page image...

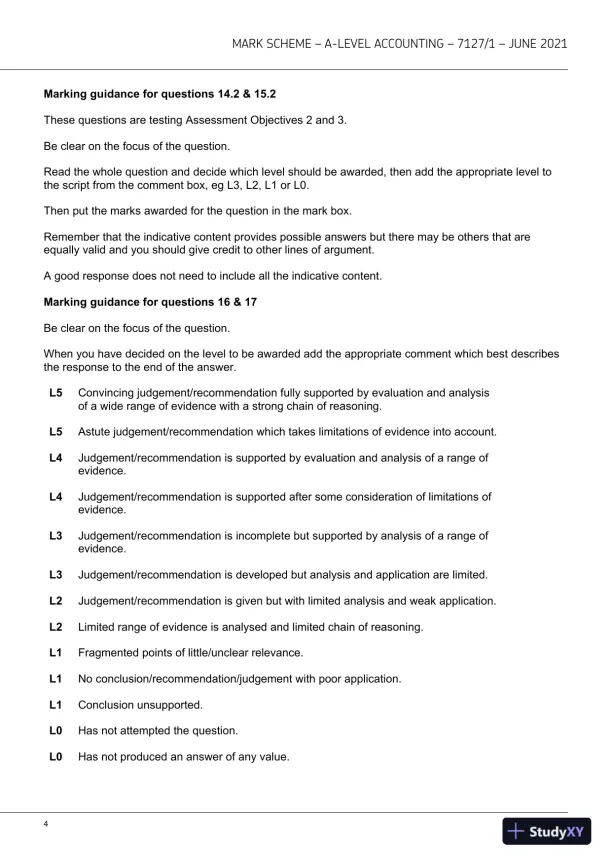

Page 4

Loading page image...

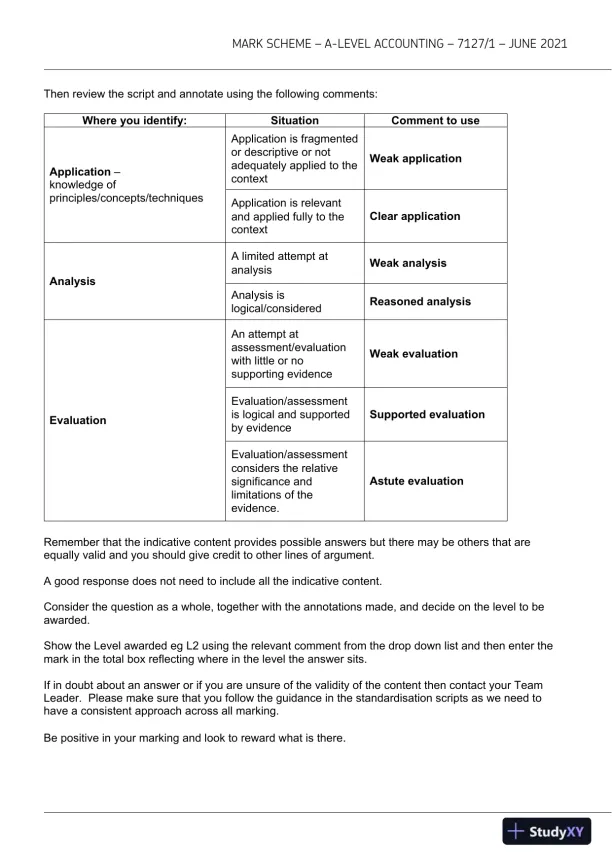

Page 5

Loading page image...

Page 6

Loading page image...

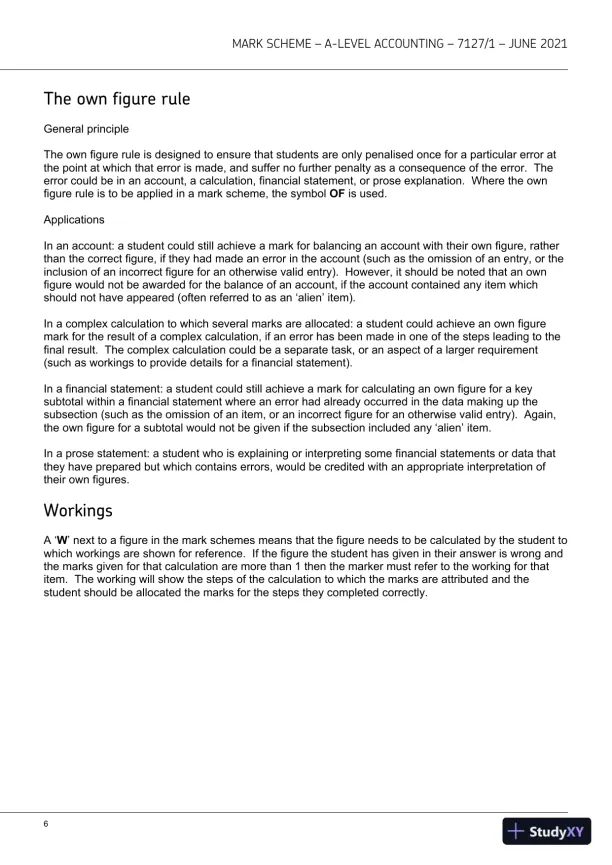

Page 7

Loading page image...

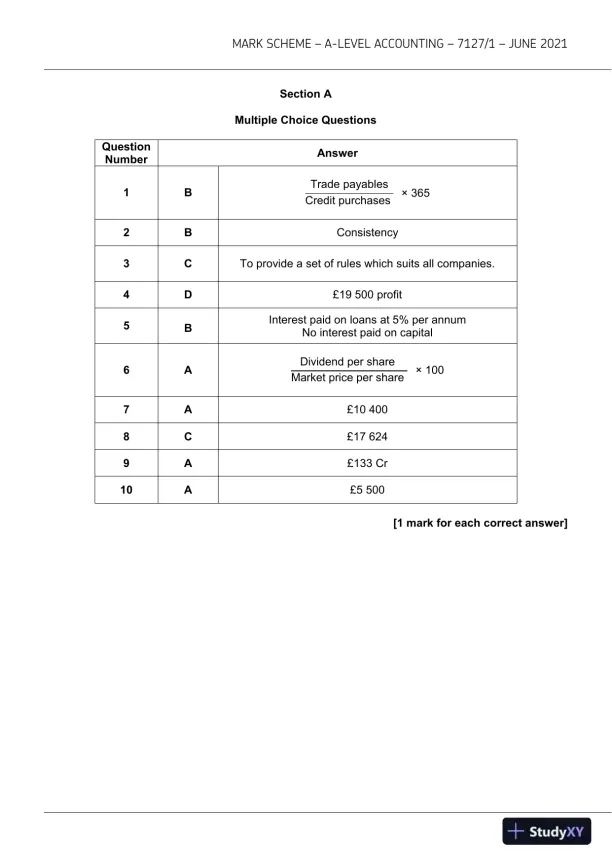

Page 8

Loading page image...

Page 9

Loading page image...